Liberated Syndication $LSYN

Subverting mainstream media by empowering creators

Quick note: while some charts are shown with data throughout the piece, most numbers used for conventional valuation work are shown in the final section

The only constant is change

The name Liberated Syndication says a lot.

A media empire can start-up today by hitting record on on iPhone. Its as simple as that.

Liberated Syndication has been there since the podcast industry started. But the industry is still relatively young.

Its cash cow, Podcast Hosting, is a commoditized business.

Competition is robust to say the least. Countless investors lose interest upon hearing there is no definitive moat.

There is no special sauce to saving data in a hard drive or uploading it seamlessly to the RSS. One benefit of commoditized businesses is that they have the benefit of highly predictable and stable demand. Podcasting has the added benefit of being an emerging trend, which means this stable demand is growing.

That’s been a nice tailwind.

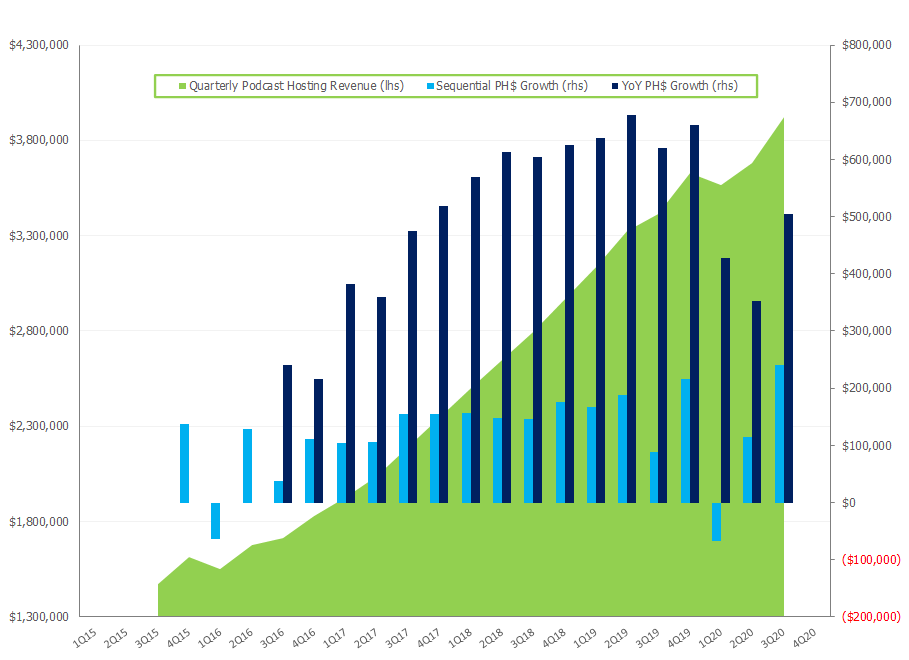

Quarterly Podcast Hosting Revenue

But Libsyn is more than just a hosting business. There is a software component. And now, thanks to new control investors with long-term orientations, the company is wrapping its commoditized hosting business with more new tools after its business was neglected by the executives that had previously been steering the ship.

There is a lot of hair here as the company has not filed a proper 10-Q or 10-K since 3Q20 as can be seen in the Podcast Hosting revenue chart above. But the new management has filed plenty of 8k-s and put out a new corporate presentation keeping us relatively up to date.

Obviously, financial statements are not where true value is created, but where it is spelled out to the financial community, so back to the matter at hand.

I think about Liberated Syndication as a sum of the parts with synergies. There is the legacy business and the potential business. The legacy podcast hosting business is key to the story and has a place as a part of the future of the company. BUT the newly acquired advertising business is faster growing and ensures the future of the company despite the competitive assault the entire podcast hosting industry is facing from Spotify which is offering free hosting. So while Libsyn’s past business is certainly important to understanding the opportunity and the industry, understanding how they are different from, and subversive to, Spotify is equally important.

What makes Libsyn subversive?

The ability to start a media empire from one’s own living room is liable to break the business model of numerous companies. More people listen to an episode of Joe Rogan than tune into CNN.

While some look down on this trend as a degradation of culture, others celebrate the downfall of gatekeepers.

Said differently, television networks are to landlines what podcasters are to cell phones. While highly produced value-add content still has a place, and perhaps a moat, there is no reason to tune in every night to watch Don Lemon lecture you on wrong-think. Personally, I enjoy irreverent commentary more than accusations of holier than thou thoughtcrime.

The internet enables people to access the best philosophers in the world on YouTube with a few clicks. Why wouldn’t policy analysis and the news follow suit?

Obviously there are many other types of podcasts out there as well from history to murder mysteries to cooking. These compete with established players for consumers time.

Newer players like Spotify, YouTube, and Facebook have gotten into the content production arena as well. However this strategy adds costs, or capital to their balance sheet, that are not necessarily accretive to their business models.

Perhaps for giants like YouTube and Facebook these costs are drops in the bucket but the idea of paying for content is antithetical to getting it for free from your users.

Spotify is already used to paying for music and its move to subsidize the hosting costs threatens to eat into the margins of podcast hosting companies.

However, I would assert that this is a rather fraught business model that Spotify is taking on. There is the subsidy they are giving to beginners for content that they are still agreeing to distribute off of their platform via RSS. But Spotify would have been able to play this content for their listeners anyway without necessarily eating the costs. Every creator would logically want their podcasts to have the reach that Spotify offers. So Spotify is intentionally increasing the capital intensity of its podcast streaming business instead of using it as a lever to offset the inherent capital intensity of streaming music.

Additionally, Spotify is now in the editorial business that has hampered Facebook and Twitter. The company has reportedly taken numerous Joe Rogan episodes down from its platform.

Joe Rogan Experience Episode #411 Conspicuously Missing

Spotify also acquired a content studio, Gimlet media. But the crown jewel, the Reply All podcast, was ultimately written off.

The company also acquired Bill Simmons’ website The Ringer, and the accompanying podcasts. This acquisition will likely go down as wildly successful.

The prior comments are not meant to say that Spotify will not ultimately be successful with producing and monetizing content behind a paywall. And while Bill Simmons’ may have been subversive to Roger Goodell he ultimately is not subversive towards the larger culture. Clearly that’s not the business Spotify wants to be in.

And this why there is plenty of room for other players in the space. Not that Libsyn has come out and stated this is the role they wish to play. But there is an opening here. Back to Libsyn’s business.

Wrapping specialized features around a commoditized offering

Advertising, which has been a historically low portion of the revenue mix, got a big jolt with the acquisition of Advertisecast for $30 million. Libsyn issued new shares to make the acquisition happen. This included direct issuance to Advertisecast’s founders and a capital raise in order to pay a cash portion of the deal.

But Libsyn went further and acquired the payment system Glow. TechCrunch reported that Glow had raised $2.3 million dollars. While this is not a lot of money Libsyn acquired Glow for $1.2 million. So lets say it was acquired for below replacement cost.

In addition to these tools that will help established podcasters monetize their media presence, Libsyn acquired AuxBus, a tool thats aimed at beginners to help them produce quality content. A funnel for new business.

The company just strapped on a newer acquisition, PODGO, which is aimed at advertising for smaller audiences. This strategy enables brands to advertise across multiple podcasts instead of dealing with individual creators with larger audiences. Ad impressions, and the ability of creators to monetize, need not be limited by having niche audiences. By being part of a larger network and infrastructure, like a TV show, Podcasters and Advertisers can still reach segmented audiences with the click of a button.

As mentioned above, Spotify’s decision to subsidize hosting costs, through its acquisition of Anchor, has turbocharged the megacap into the podcast space.

Spotify is one of many competitors in the space. YouTube has been in the space for a long time. Substack (thanks for this platform!), Patreon, and SuperCast are newer companies on the scene with clean interfaces that allow creators to do interesting things. Legacy players include blubrry and buzzsprout.

As stated earlier, Podcast Hosting is a commoditized business. This is not necessarily bad as it means there is stable demand, which is still growing.

The acquisition of Glow and Advertisecast show us that Podcast Hosting’s cash flows are being reinvested into lowering churn among existing podcasters by helping them monetize and creating new business lines.

A Differentiated Opinion

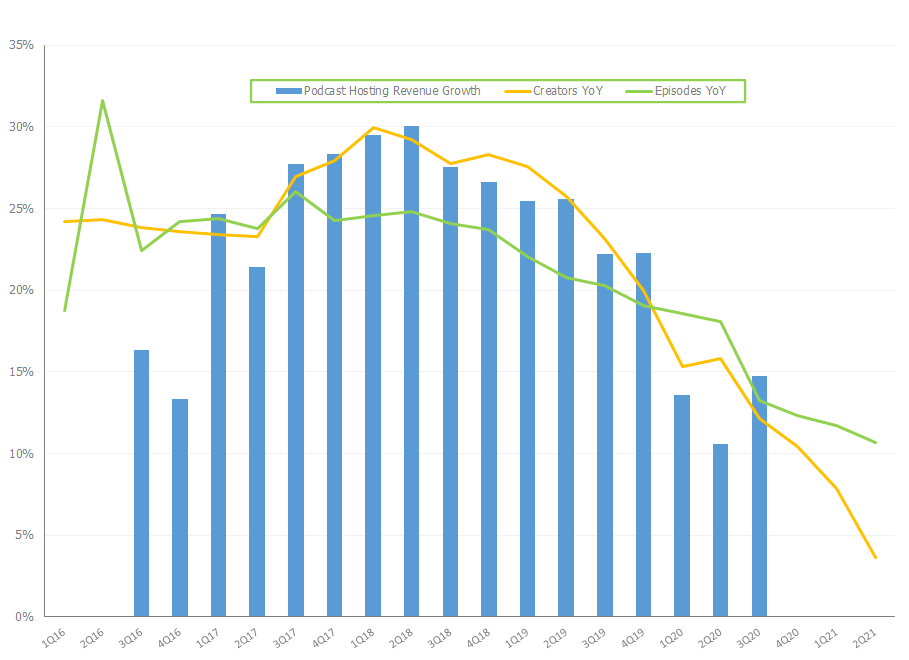

Obviously it is in every shareholders interest to see Podcast Hosting revenues continue to increase. Adding new creators is a straightforward way to accomplish this. However, in all likelihood, high margins within a highly competitive and commoditized industry should logically decrease over time.

Revenue growth has slowed consistently in percentage terms since 2018. Although above we showed growth in dollar terms looks more stable and appeared to be recovering from a drop in growth during lockdowns.

Quarterly Podcast Hosting Revenue

At the very least, episodes recorded are still growing at a faster rate than new creators. This is positive if you think about the monetization from the perspective of the Pareto Principle. The biggest stars will ultimately produce the lions share of cash in the ecosystem.

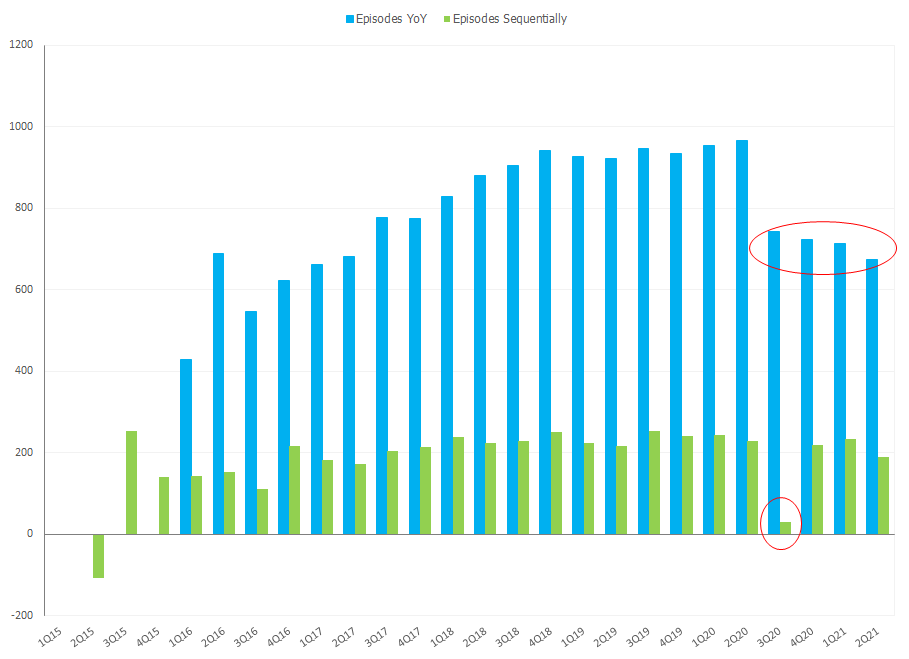

Episode Growth YoY is Distorted by One Poor Quarter

More prolific creators with more storage needs are one avenue for growing ARPU.

This is not to dismiss concerns around slowing growth of creators. Besides generating immediate revenue which every investor obviously cares for, onboarding new creators is obviously an amazing funnel for recruiting up and coming stars.

However, Anchor’s decision to offer free hosting is a significant competitive headwind. Clearly its not management’s fault that Spotify is choosing to run the cost of hosting to zero. And management has responded by skating to where the puck is going.

Running the costs to zero themselves does not make sense either. I would argue more subversive stars are highly motivated to keep their content hosted by more neutral parties than Spotify, who have shown a propensity to moderate content. There are also enterprises that utilize Libsyn. Do you really think companies such as Deloitte, Ebay, and Forbes with large operating budgets and staffs that are comfortable using the Libsyn platform are going to change providers? I don’t think so.

Podcasting also competes with Netflix, YouTube, Radio, TV, and music for listeners’ attention. This helps put future monetization strategies into perspective.

While capturing new creators is great, capturing existing creators who are already monetizing is better. Libsyn appears to think it can do both, but focusing on creating the best platform for established and talented podcasters is a much better strategy.

The Netflix comparison is helpful here, obviously Dave Chappelle gets paid more, and brings more fans to Netflix than the series The Standups. It doesn’t mean Libsyn should not strive to onboard newer emerging talent as well, but focusing the company’s resources on established creators makes the most sense.

New creators are welcomed to the platform but going forward the true elephants worth hunting for are the biggest podcasters who get the lions share of listener attention. These creators will sell the most ads, though admittedly may not require that much help from Libsyn to do so.

This is a challenge for the entire industry. Why would the biggest creators need help placing ads? Many are read live on the show by podcasters. Bill Burr once lost an advertiser for making jokes about issues surrounding gambling. He turned the ad into more content, and has less issues around other products such as underwear. This is an example of the the best talent having integrity around monetization.

Still, Libsyn offers the ability to save podcasters time by having pre-recorded ads that can be dynamically changed by location and time, more akin to television.

There will always be a cohort of creators who prefer zero advertisements. These creators can utilize Glow for private feeds.

The investors who run the company are aware of the competition they face from companies like Patreon that offer a Walled Garden social media component to their business.

With Glow, this is the next logical component for the company to penetrate. Patreon still intermediates podcasters’ relationship with their own app.

For Libsyn, white labeling private applications for creators would allow them to completely own the relationship with their listeners and magnify their brand.

How should we think about valuing Libsyn?

(This section is qualitative with more quantitative statistics in the following section)

The power of the internet and the fraying moat of network television bring up a few questions.

Is Libsyn a tech company? Are they a media company? Are they an ad-agency? Ultimately, I think the most positive way to think about Libsyn is as a company that Barry Diller and Joey Levin may think about getting their hands on.

Podcasts are interactive media. That’s how Patreon and SuperCast are doing it. Its how YouTube has always done it. Its the next logical step.

Supercast Ask Me Anything Feature

Audiences get a sense of community from listening to podcasts and this is a gigantic opportunity.

Management is, at the very least, aware of the Patreon comp and opportunity. I cannot say whether Walled Gardens are a surefire product extension, but it is the logical next step after acquiring Glow.

The company’s business model is superior to others that pay to produce content. While Spotify is clearly suited to do this since their main Music business already necessitates it, its a more asset heavy approach.

Lastly, I would state that the controlling shareholders seems to be extremely thoughtful. They are currently suing to cancel over 7 million shares. They recently cancelled over 1 million shares from the former CEO.

One controlling shareholder seems to have found alpha in his career in the legal system, winning a lawsuit against the Government of Mongolia. Looking at his portfolio you can see that he has a current holding of a Venezuelan Gold company. So in handicapping the case, we can say that the lawsuit is not exactly a moonshot. Especially when you consider that the case is against Chinese shareholders that were accused of obtaining their shares by lying to Libsyn about their assets and subscribers. Even if the case fails, management should be given credit for pursuing it.

Beyond the legal alpha, the current CEO is also an investor who’s worked at Credit Suisse First Boston and Caxton Associates. Considering the company has leaned on a lot of M&A, and raised capital to do it, having investors at the helm is reassuring.

Putting some numbers to it (and some more words)

Below I show the company’s free cash flow in 2018 and 2019. I adjust both lower by $1 million because Libsyn has had to settled tax issues on behalf of the old executive team of Libsyn which did not do basic finance and accounting work. Still the Free Cash Flow margins are strong. I left 2020 blank since we do not have financials filed.

Below the Free Cash Margins I add in Advertisecast revenues over the past three years. While I do not know what those margins are the growth is clearly robust in this segment and looks like it will eventually eclipse podcast hosting revenue.

The 2020 revenue shown below is LTM of disclosed revenue for Libsyn through 9/30/20. Podcast Hosting revenue was 59% of that number at around $14.8 million.

Although creator and episode growth slowed, as shown earlier, they still grew. So that should imply some form of growth in 2021.

While I did not really cover the balance of existing revenue besides Podcast Hosting in this piece, it was largely website hosting and a smaller existing advertising business.

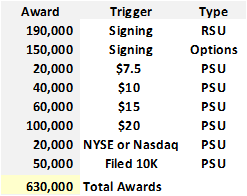

The approximate diluted share count is the outstanding share count on the bottom of the front page of the 9/30/20 10Q + shares issued to acquire Advertisecast + CEO + CFO + COO stock grants that have been issued since that time. It is a rough approximation but the CEO’s comp is extremely interesting, and shown below.

Bradley Tirpak, CEO compensation rewards performance

Besides share price performance awards, filing the 10K and uplistings both work to increase liquidity in the shares. The shares currently do not trade often since the SEC stopped allowing prices to be quoted due to their out of date financials.

My favorite comp for Libsyn is Patreon. Patreon was reportedly valued at $4 billion after raising $155 million dollars from the likes of Tiger Global and Wellington. That’s more than Libsyn’s market cap.

According to Patreon, its 200,000 creators across podcasts, videos, music, visual art, writing and more are earning over $100 million per month from 7 million patrons.

Patreon’s creators have earned more than $2bn since the company’s inception in 2013.

$100 million dollars a month that they earn a take rate on sets up a nice recurring revenue stream. However, I personally listen to two podcasts hosted on Patreon. Both have been discussing leaving the platform for, admittedly, an extended period of time over basic missing features such as the ability to comp memberships and very high fees.

Libsyn currently has 75,000+ podcasters, so ~1/3 of Patreon. If Libsyn utilizes its current cash flow to fund operations and offer a lower take rate they are looking at a great opportunity to win over creators and hire a large developer team to build white labeled turn key applications. This would give podcasters the branding, technology, and multiple monetization tools to start media empires.

Substack raised money around the same time as Patreon at a more modest $650 million valuation. The company is younger, but at least on Fintwit it seems to be bursting at the seems. The company has announced extremely exciting ways to support its writers by offering legal support for journalists and healthcare options even more recently.

Is the whole worth more than the parts?

Above I show basic valuation frameworks for the legacy business and the Advertisecast business. The 2021 estimate for cash flow adds modest 5% revenue growth to 3Q20’s revenue run rate and uses the higher 2018 free cash flow margin shown above, because FY2019 was weighed down with legal costs. While I’m not crazy enough to value the legacy hosting business at 17x sales multiple like AWS, this is a hosting business. Unfortunately, Spotify does limit the ability to value it higher here.

Advertisecast was acquired for a 2.5x sales multiple of 2020’s revenues. If 80% of advertising revenues ultimately come from 20% of your creators the addition of PODGO should help the advertising efficiently monetize the remaining 20% of ad dollars in a way that may not have been possible otherwise. This calls for at least a 20% increase in the multiple of this business, perhaps more. At the very least, it should ensure the growth rate in this secularly growing section of the ad market doesn’t slow down too much from 2020’s ~45% growth.

This framework offers a margin of safety which utilizes tame multiples.

Share Count and Pro Forma Valuations show my analysis is likely too harsh on the legacy business

Combining this margin of safety with highly engaged investors and the strategic value 75,000 podcasters have to bigger companies that want to get their foot into the podcasting industry means much more upside. Another path towards excess returns would be if the company was valued as a SaaS business and rerates due to the software component that makes its hosting service sticky to customers.

Value you it how you will. I have already made clear serious option value should be assigned to Glow. Between Patreon, Substack, Supercast, and even Twitter’s new tools the TAM for creators directly monetizing is growing.

A large part of the value in my opinion derives from savvy creators valuing a robust ecosystem more than negligible costs to host their podcasts being run to zero. Spotify is big tech and has already shown itself to be censorious. This urge to censor is driven by real angst among the online community, but its also driving real angst among creators that frankly has led to so much of Substack’s success. Let one of the founders of Substack set the stage:

The angst that people are feeling is not coming from nothing.

Because of the feeling that this stuff is driving us all crazy, there's this increasing sense of like “Oh God, oh God, somebody has to do something.” And this — censorship — is something, therefore we must censor. I think the pressures there is like, well, these companies should be doing lots of good censorship to make sure that bad things don’t happen, or maybe the government should be forcing them to, or maybe they shouldn't be doing it because then they have too much power, but the government should be doing it because good God, somebody has to have control of all this stuff!

There is strategic value to the success of smaller players to the podcast ecosystem and this is why direct subscriptions could ultimately be more valuable to Libsyn and its creators than the advertising model. They insulate creators from the 24 hour news cycle. But even more importantly, from the the founder of Substack once again:

People tend to think about this like, “I could make money with ads. I could make money with subscriptions. Two moneys is better than one money.” But when you’re making the best possible product to drive subscriptions, what you end up having to write is qualitatively different — and better — than the thing you’d have to do to drive the most ad revenue.