Thiel’s quote is about the best quote I can find to describe the scope of what Josh Crumb, the founder of Abaxx, is setting out to accomplish.

Worldbuilder or Bust

Abaxx has three main business lines currently under development that it will be engaged in as a public company.

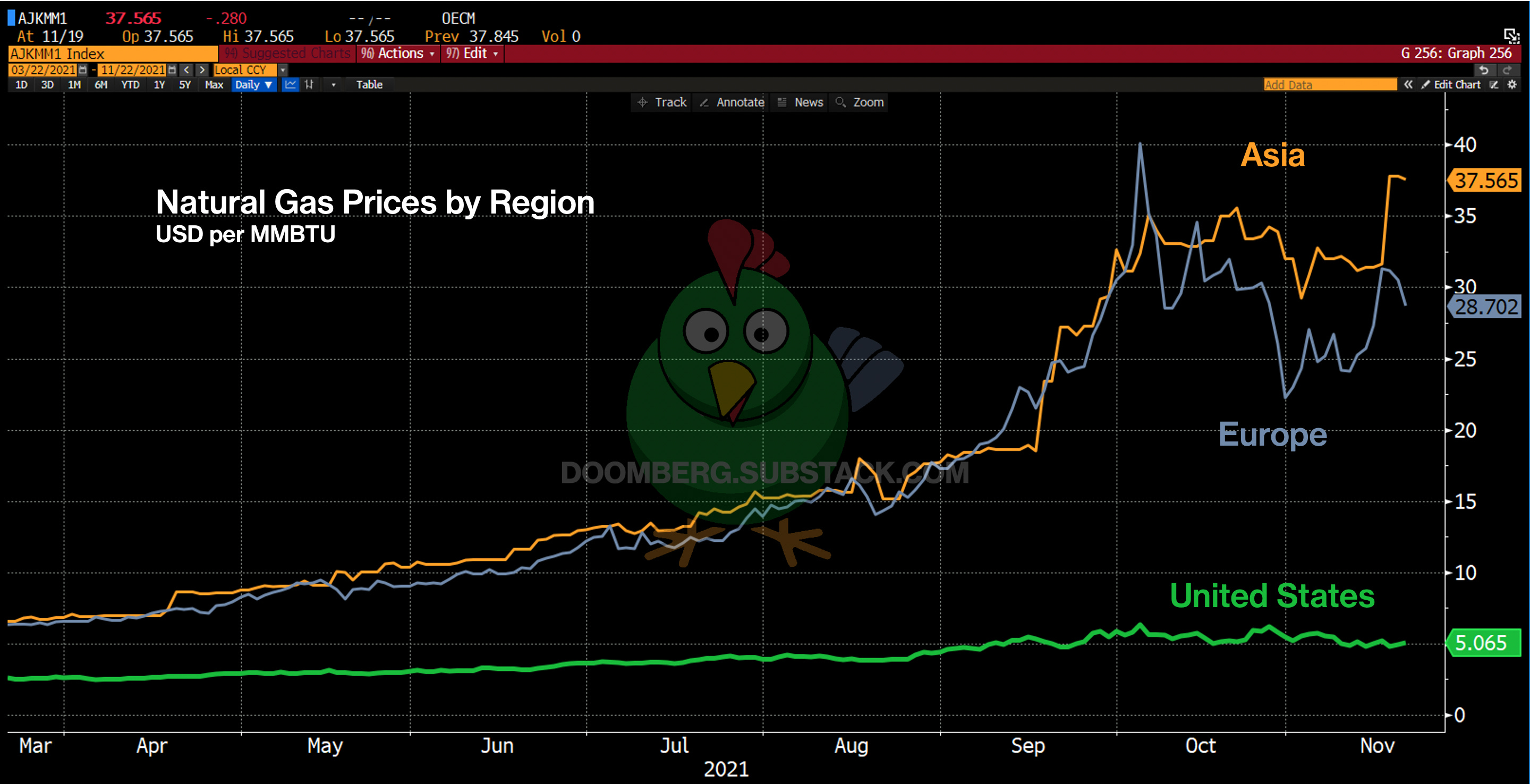

The company is launching a commodity exchange and clearinghouse in Singapore that will focus on the physical delivery of Liquefied Natural Gas, or LNG for short. Natural Gas has been touted for its low cost and for being a relatively cleaner burning fossil fuel than alternatives such as coal or oil. The company hopes to create the WTI index of LNG. This sort of index would be a lucrative business on its own that could earn the company royalties beyond its exchange function. The exchange is also launching a gold contract, and will roll out other contracts focused on battery metals in the future.

“The Abaxx technology captures and disseminates transparent transaction information, enabling traders to bring more certainty and to more easily verify criteria supporting all aspects of ESG transactions… Our ESG-ID technology provides the market unique capability to 1. Measure, 2. Verify, and 3. Report compliance with global standards (carbon footprint, social metrics, fair trade, child labor, conflict zone, etc).”

The company is building a technology stack for decentralized identity services called ID++. These technologies will be utilized by traders and end users on the exchange for services as wide-ranging as video and text chat and document signing. This technology will utilize the blockchain, NFTs and already has signed some related-party agreements.

In a lot of ways Abaxx is skating to where the puck is going, which is ironically a little less subversive.

Josh’s access to capital has enabled him to use Abaxx’s balance sheet as a platform for making several investments. These investments are ESG focused and will utilize the company’s technology. This investment activity could also be described as the a fourth business line, though it really focused on business development for the main business lines. As these companies raise more outside capital, and Abaxx spins off part of its stakes in these businesses the technology revenue Abaxx generates will become less incestuous and provide valuable use cases for this line of Abaxx’s business. Some use cases Josh has spoken to include contracts that utilize NFTs, e-signatures, and encrypted messaging. But even wider ranging, Josh hopes that when you log into a website in the future, Abaxx can act as your digital identifier. This would allow users to avoid having numerous accounts all over the web.

Investments in AirCarbon Exchange and BASE Carbon are high probability ways to profit from the ESG phenomenon that has taken markets by storm. Investing in a carbon exchange is easy to understand, for a company that was founded to launch its own exchange. BASE Carbon, is upstream in the carbon value chain and will utilize its own balance sheet to create carbon assets that will trade on the AirCarbon Exchange creating something of a flywheel.

Josh, the CEO, seems intent on making positively impactful investments as opposed to the majority of the ESG industrial complex which spends an inordinate amount of time focusing on their image. Perhaps absorbing capital that could otherwise flow to these gigantic corporates hoping to leech new flows of capital is a bit subversive after all.

While capital formation is what capital markets are all about, a better way to think about Abaxx is as a capital facilitator. As a seasoned financial professional Josh has marshaled resources from an impressive investor list and has used his start-up as a vehicle to make its own seed investments.

The two biggest name investors on board are Robert Friedland and Kyle Bass. Both have their own designs on how they can profit from this company.

Going further, through Abaxx Josh is facilitating a Realpolitik initiative to reduce carbon emissions globally. While institutions like Blackrock rush to repackage ETFs with the likes of Apple and Microsoft with ESG wrappers Abaxx is looking to facilitate the flow and use of energy towards a suitable base load power source, Liquefied Natural Gas (LNG) that emits less carbon and other pollutants than coal.

A bridge as a bridge

Abaxx is starting a full stack physical commodity exchange in Singapore. The company’s plan to launch it has already been set back a couple times due to the approval process taking longer than expected, but the company has Approval in Principal for both its exchange and clearing functions in place.

Josh has specified that Abaxx will be focusing on physical settlement. This is a big deal. For a lot of exchanges their primary customers are financial speculators. There is nothing wrong with financial speculation. But speculators are ultimately in the business of predicting mispricings in reality. Contracts that never physically settle do not inform people as to what stuff is needed where.

Its unfortunate that the exchange was not able to open on schedule, as you can imagine volume being huge with the crazy increases in energy prices and volatility this year. Perhaps the exchange could have eased some of the volatility.

Doomberg, the Paranoid chicken wrote:

Exchanges backed by physical product are a marvel of markets. They facilitate standardization of product and price, enable efficient planning for producers and consumers alike, and create venues for speculators that allow transmission of market signals into the real economy. In the long run, physical exchanges lower the price and increase the use of the underlying commodity being traded.

That is the hope for LNG. Importantly, looking at the chart below, while Coal has lost market share as a percentage of the overall energy market, the amount of Coal being utilized has continued to increase over time! This is even as the US has switched high amounts of Coal burning power utilization to Gas.

The implications of this for the global economy are gigantic. Humans’ energy consumption will continue to grow. Poor countries will not sacrifice their human dignity and living standards to climate change fears, when poverty already kills people today.

However unlike many pie the sky calls for renewables, which actually *destabilize* energy grids, natural gas is the low hanging fruit that can take the world to less emissions and FAST.

Lately Uranium has been ripping as Nuclear investments and popularity have gained steam. This is deserved. But the problem with Nuclear energy is the capital intensity to build plants. While modular plants are in the works to fix this, its still in an experimental phase, meanwhile Uranium supply is not ready to meet the projected needs even before announced incremental investments.

via Sprott

Goehring & Rozencwajg have done a lot of work on the Energy Return on Investment or EROI. Its pretty clear that renewables are not up to the task of replacing coal, especially for poor nations.

In its outlook for 2021 LNG demand Shell wrote:

[G]lobal demand for liquefied natural gas (LNG) increased to 360 million tonnes. Though marginal, the increase in volume reflects the resilience and flexibility of the global LNG market in 2020, a year which saw losses to global GDP of several trillion dollars as economies large and small struggled to contain the COVID-19 outbreak. Demand in 2019 stood at 358 million tonnes.

China and India led the recovery in demand for LNG following the outbreak of the pandemic with both countries increasing their LNG imports by 11%. China’s announcement of a target to become carbon neutral by 2060 is expected to continue driving up its LNG demand through the key role gas can play in decarbonising hard-to-abate sectors. India increased imports, as it took advantage of lower-priced LNG to supplement its domestic gas production. Demand in Europe, alongside flexible US supply, helped to balance the global LNG market in the first half of 2020. However, supply outages in other supply basins, structural constraints and extreme weather later in the year resulted in higher prices.

Global LNG demand is expected to reach 700 million tonnes by 2040, according to forecasts, as demand for natural gas continues to grow strongly in Asia and gains further traction in powering hard-to-electrify sectors. As a result, more supply investment will be needed to avoid the estimated supply demand gap in the middle of the current decade.

So the demand for Natural Gas is feared to be so immense that there will not be enough supply! That’s already a fear today, with prices soaring and energy retailers in the UK continuously going out of business. Now imagine an exchange that focused on physical delivery being there to fill that gap! The opportunity is enormous. US producers/exporters already knew about this opportunity before prices surged.

The availability of future contracts will allow for O&G management teams the world over to plan investments and justify capital investment. It will allow utilities to take the other side and lock in profitable rates to their customers in advance.

Doomberg agrees:

Because of the intense need for infrastructure investment to unlock its utility, the natural gas market is highly regionalized and surprisingly heterogenous. Substantial and durable price differences are common between geographies and even within countries. As described in a prior piece, we are endlessly fascinated with such arbitrage situations and how they drive significant innovation.

This type of exchange could also ease Europe’s dependence on Putin’s Gazprom for energy. The implications are exciting to say the least. And the team Josh Crumb has put together is formidable.

Abaxx has a team of alums from Goldman Sachs, NYMEX, CME, ICE, Singapore/Hong Kong mercantile exchanges, among other institutions.

This large, well-rounded team is poised to execute with the help of Nasdaq’s matching technology which lowers execution risk.

Lets repeat that last point.

Abaxx partnered with Nasdaq in building its own matching technology.Abaxx has worked diligently to get regulatory approval from the Monetary Authority of Singapore, is currently selling its technology stack to numerous younger staged companies BUT is humble enough to take minimal operational risk when it comes to executing trades.

Fossil Fuels are basically table stakes to participating in global commerce, but setting up this Natural Gas Exchange is probably not how most climate activists imagine the global energy transition to take place. Josh does have plans to move into battery metals and down the line we will see other base metals, like copper, that are needed for electric cars and grid modernization trade on the exchange too.

Robert Friedland has spoken to his hopes that NFTs will be able to track commodities around the globe, so that consumers can be sure how ethically sourced their products are. This could equal more products to trade on the Abaxx Exchange. There will be a copper contract, and a premium copper contract for Veblen commodity goods.

Acting as a bridge to a cleaner future is exciting, and profitable enough, but the exchange is also a bridge towards capitalizing on what is a much more subversive goal. Josh’s ID++ technology.

Identity as an Industry

This is an industry that has immense potential. Current tech giants and financial institutions have a serious advantage due to gigantic user bases numbering billions. Smaller competitors exist as well, such as the airport security company Clear and Mitek systems.

I really do not want to attribute too much value to this piece of the business because it does seem like a gigantic moonshot. However I do want to point out a few reasons why I find the opportunity compelling and will be happy to be proven wrong.

In an “Abaxx Twitter Analyst Spaces” hosted by GRIT Capital, Josh noted that there was no reason for everyone to be accessing the conversation via Twitter Spaces. This is reminiscent of when Xbox and Playstation would prevent Fifa players from playing each other.

There is no reason that participants should not have been plugged into the conversation through various applications, ranging from Clubhouse, Twitter Spaces, to an Abaxx facilitated platform. There is a distinction here between Platforms which seek to force users into a specific playpen and Protocols which would allow for more fragmented connectivity.

While Abaxx may be able to onboard users to this decentralized Web3.0 login through its exchanges and other investments that it has made, this extremely subversive business is much more speculative than the exchange.

Traders on the exchange will be able to use this tech to sign contracts, send messages and video chat.

Josh has derisked the ability to speculateand participate on the upside of this opportunity working out, however the value creation that makes this possible is the commodities exchange, so lets get back to Abaxx Singapore.

Owning the Bazaar

Exchanges are phenomenal businesses.

I am not an exchange expert by any means, so I will paraphrase a bigger investment firm than myself, in case it is important to the reader:

Oppenheimer described the industry as oligopolistic. They went further in comparing these types of businesses as similar to Mastercard or Visa due to the matching of sellers and buyers. The final point I will hammer home from Oppenheimer is the incremental capital needs are low. Once these businesses are established and growing revenue they are valued extremely richly since they do not require a lot of capital to be reinvested.

The ability to own a capital light oligopoly BEFORE its appreciated by the market is available to anyone who will open their eyes to the opportunity.

Going further, Abaxx is looking to establish its LNG contract as the global benchmark similar to WTI for oil. This would open the opportunity to licensing out the benchmark.

The only thing that gives me pause here are the regulatory requirements of clearinghouses to hold capital on balance sheet. And while I am no industry expert, CME has a clearing business and serially returns capital.

I am not saying to expect the Abaxx Exchange to return capital soon after it launches. I am just trying to demonstrate why these businesses are highly valued. Though, Abaxx is spinning off its investment in BASE Carbon.

Trust but Verify

In the company’s latest investor deck they highlight that Robert Friedland owns 6.7% of the company. In fact I took the “Owning the bazaar” line entitling the previous section from him. He is also the entrepreneur behind Ivanhoe Mines, a copper miner, as well as Ivanhoe Acquisition Corp, a SPAC taking a lithium battery company public.

Beyond the fantastic economics of exchanges, he is hoping to leverage Abaxx’s technology to “grade” his minerals as ESG. This use case may utilize non-fungible tokens (NFTs) at scale for commercial purposes.

The value and implications of this technology are gigantic. While what is possible and what are probable are often two completely different outcomes, Friedland hopes that if he mines copper in the Congo it will trade at a premium to another mine that uses child labor.

Base Carbon, a Carbon Credit ‘Manufacturer,’ has already licensed this technology “that would pay Abaxx a 2.5% royalty on gross revenue for previous financial assistance and the usage of software it developed. The royalty is indefinite in term and Base Carbon has the right to buy back the royalty upon the payment of US$150 million to Abaxx.”

Below is an image produced by Abaxx investor James Duade:

Abaxx’s investors own a piece of every link in this chain. I do not want to attribute too much value to this ‘Measure, Verify, and Report’ business line in terms of valuation but it does speak to the lengths Abaxx has gone to earn investor trust. If global investors are truly interested in ESG standards, Abaxx is working hard to bring integrity to the market.

No greenwashing here.

Going further, if Abaxx can grade commodities and verify the quality of Carbon Credits, what is to stop a Utility from earning Carbon Credits by switching baseload power from Coal to Natural Gas? Such a change could require poorer nations with lower living standards to invest additional capital. Rewarding them with Carbon Credits seems like a natural incentive for good behavior. Verified using Abaxx technology of course.

What Makes Abaxx Subversive

So far we have discussed business lines that seem to be extremely in vogue. However this company has very subversive roots.

Exhibit A is a slide from their most recent investor deck highlighting the Gold Contract the company is launching:

Much ink has been spilled in endless screeds and tirades lambasting the London Bullion Market Association (LBMA). The research department at Goldmoney where Josh used to be CFO was certainly not an exception here.

Typical complaints about the LBMA come down to the price of gold being suppressed due to the rehypothecation of the precious metal. At the very least the previously mentioned ‘Measure, Verify, and Report’ software systems will ensure that Carbon Credits are not double counted.

No free green lunches.

But back to the Gold market. Claims that the Bank of England, UBS, and other giant financial institutions endlessly lend gold back and forth so no one is ever caught short are a frequent charge in the goldbug community. Perhaps Josh thinks setting up this exchange could have some sort of impact on these market dynamics. Maybe I’m thinking to much into it.

But here’s what I do know. Abaxx is focused on physical delivery in a financialized global economy where many futures exchange contracts are cash settled. Below I have a part of a twitter thread by the account @hidenotslide, an expert/investor in exchanges, who discusses how so many products are formulated on exchanges today:

Imagine you're a large, established TradFi futures exchange. You make money by collecting trading fees on your large portfolio of futures products in a variety of asset classes. Where do you get ideas for new products? Your institutional customers.

An idea for a new futures product normally comes during conversations between an institution & an exchange salesperson/account manager. It normally sounds like this: "Man, we really think we could trade XYZ futures product in large size if it was available. Can you build it?"

This idea goes from the salesperson through a series of approvals by their boss, their boss's boss and/or a resource committee. Each ring on the approval chain creates a space where the initial idea can be blocked or altered from the original ask, like a game of Telephone.

If the idea passes through these approvals it gets to the design phase, normally a conversation between the sales & product teams.

The process goes on and on. The point being that current exchanges are more focused on financial players, like macro hedge funds than end users. That’s not subversive.

Josh took the inverse approach. This highlights the value this company is looking to create in the real economy all while coloring within the lines of the Monetary Authority of Singapore.

Valuing an Oligopoly

I’m going to start by giving another shout out to James Duade who has been the absolute axe on this name. He came to it from a much different place from me. I followed Josh to this opportunity. From what I can tell, James was previously invested in the predecessor company New Millennium, which *still* owns an iron ore deposit.

Taking this deposit, the value of Base Carbon and other investments, the exchange licenses/infrastructure (that take a significant time to earn approval) and the company actually has a nice margin of safety. But that’s not why I wrote this piece.

We are elephant hunting. The point here is to own one of the best business models in the world BEFORE others recognize the opportunity. Are we taking risk here? Absolutely.

But given the enormous market need and turbulence in natural gas prices this year an the LNG Exchange looks to be perfectly timed. Plus Asia is overtaking Europe as the largest importer of LNG gas which makes Singapore a great locale.

In the company’s presentation the company lists its estimate for industry revenue as the “Medium-term LNG derivative TAM” of $500mm. The company has the following footnote:

“1) LNG Market revenue calculated based on assumptions: Production of 10,000 lots/day x Trading (Notional) of 50x = 500,000 trades/day. Daily revenue of ~US$3-5mm/day.”

Its not exactly rocket science that at the low end, the company’s guidance for the long-term opportunity is actually 50% bigger than the “Medium-term”. At the high end its a 150% bigger TAM.

So how should we value this LNG opportunity? Below is a simple framework using a 11.25x sales multiple as a base case. Abaxx Technologies owns 91% of Abaxx Singapore, so below in gray is the value of the exchange to shareholders. On top of this Exchange value to shareholders, Abaxx Technologies earns royalties bringing the actual economic value to $ABXXF shareholders to somewhere between the white and gray values.

The 11.25x sales multiple is a rough average of the CME, Nasdaq, ICE, and CBOE BEst estimates from Bloomberg.

I can imagine cogent cases for both a lower or higher multiple. A lower multiple can be argued for because the company’s valuation may not be supported by earnings up front, unlike these established companies. On the other hand I valued Abaxx Singapore solely on its LNG contract. We know they are also rolling out a gold contract, a gigantic market. We know they are planning on battery metals.

Ultimately, Josh and many of the company’s backers are not some pie in the sky Silicon Valley types that want profitless growth for growth’s sake. We can count on the team to run the business rationally and profitably.

The fully-diluted share count listed in the company’s latest prospectus is 80.5 million. Josh owns over 11 million.

We also know they are ESG. Listen, I’m not counting on investment flows to get my money back. I’m not invested in Rivian. But extra investment flows are welcomed.

Ultimately there is a lot of optionality in this name beyond the exchange. Its not my expectation, but I’m ok with them expiring worthless, as long as I end up an oligopolist.

I get that this could be an asymmetric bet, but why do you think one of the established exchanges aren’t trying to enter the same space? This is a not a retail punter space, so why would established trading houses, utilities, lng producers etc ever consider placing trades on a start up exchange? Come to think about it, why aren’t Glencore, Vitol and the like on abaxx’s shareholder list?

Awesome write up and pairing with James' work on Abaxx. How are you thinking about the time horizon for this investment? It is such early days for the company so is this a decade long buy & hold?

I get that this could be an asymmetric bet, but why do you think one of the established exchanges aren’t trying to enter the same space? This is a not a retail punter space, so why would established trading houses, utilities, lng producers etc ever consider placing trades on a start up exchange? Come to think about it, why aren’t Glencore, Vitol and the like on abaxx’s shareholder list?

Awesome write up and pairing with James' work on Abaxx. How are you thinking about the time horizon for this investment? It is such early days for the company so is this a decade long buy & hold?